The European Union’s new VSME standard (Voluntary Standard for non-listed Micro, Small, and Medium-Sized Enterprises) is intended for SMEs that are not subject to the CSRD directive but wish to report on their sustainability. The aim of the standard is to provide stakeholders with information on the company’s sustainability performance, as well as to improve internal sustainability management and access to finance. All of these goals sound promising, but unfortunately, the standard falls far short of the real needs of SMEs and their stakeholders.

In the daily reality of SMEs, sustainability work is largely built on the values of entrepreneurs and companies, the operating environment, and practical actions—areas the VSME standard hardly addresses. Instead, the reporting focuses on extensive data points that do not necessarily support the concrete sustainability efforts of SMEs. This makes the standard impractical and, at worst, a misleading tool for small and medium-sized enterprises.

This makes the standard impractical and, at worst, a misleading tool for small and medium-sized enterprises

–

Disconnected from the everyday reality of businesses

SMEs practice sustainability as part of their daily operations – through energy efficiency, resource savings, promoting employee well-being, and transparent business practices. Integrating these themes into business development is what ultimately makes sustainability impactful.

The structure of the VSME, on the other hand, separates sustainability into a standalone reporting task, which does not necessarily support the strategic development of the business. The standard also fails to recognize that sustainability work in SMEs is deeply connected to the core business, company values, and operating environment.

–

The irrelevance of biodiversity data points

The VSME includes data points related to biodiversity (e.g., the company’s location near protected areas). However, this does not encourage SMEs to take concrete actions to mitigate biodiversity loss, but rather to document a passive state.

SMEs have many ways to influence biodiversity – for example, through responsibility criteria in the supply chain, improving the sustainability of procurement, and developing their own operating practices. However, the standard does not address these aspects.

–

Social responsibility – nothing but gender distribution?

The social responsibility section of the VSME focuses largely on gender distribution and equality issues within companies. While these are important topics, they do not come close to covering the full scope of social responsibility in SMEs, nor are they at the core of it.

In the daily reality of SMEs, social responsibility means supporting employee well-being, occupational health, skills development, working time arrangements, flexibility, and a positive employer image. However, the standard does not provide guidance on these aspects.

–

Strategic sustainability work is missing

Sustainability work should support the company’s strategy and business development. However, the VSME does not offer any concrete tools for setting sustainability goals or measuring them, other than mentioning them in passing. This makes the standard more of an administrative reporting obligation than a genuine tool for developing sustainability work.

In SMEs, sustainability goals must be clear, measurable, and linked to the business. Without this, sustainability work remains disconnected and does not generate long-term added value for the company.

–

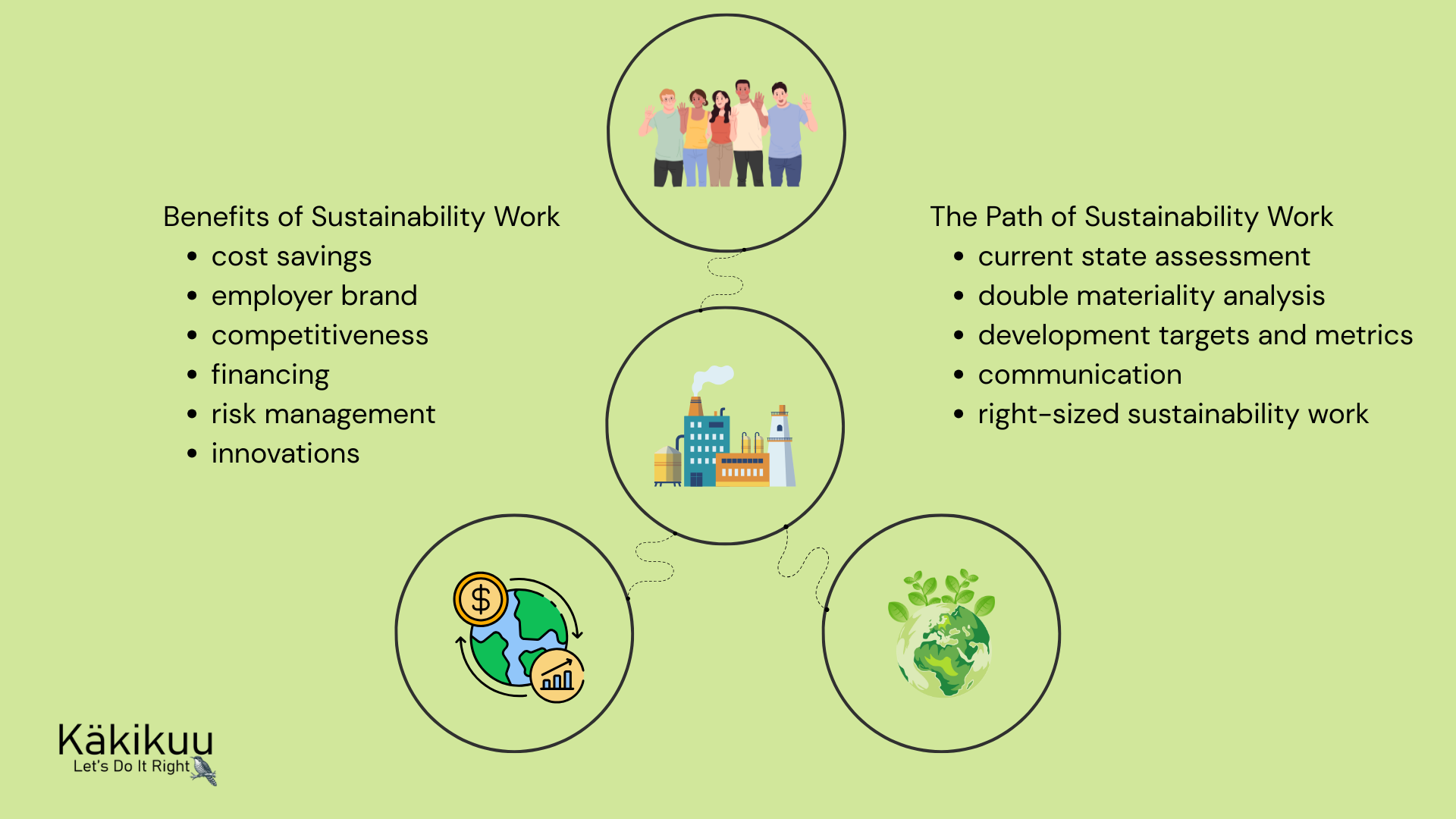

How should SMEs proceed?

I continue to recommend that SMEs focus on building sustainability work that is integrated into their business operations. This means, among other things:

- A sustainability plan based on double materiality assessment – which sustainability themes are material to the business? How does sustainability support the company’s growth and competitiveness?

- Concrete, measurable goals – sustainability work should be built systematically so that the set goals are achievable and measurable.

- Stakeholder involvement – customers, employees, and partners should be included in sustainability work, as their expectations influence the success of the business.

SMEs do not need more bureaucracy and reporting burden, but impactful and strategic sustainability work that supports the business.

SMEs do not need more bureaucracy and reporting burden, but impactful and strategic sustainability work that supports the business.

The VSME is intended as a simplified version of the EU’s Corporate Sustainability Reporting Directive (CSRD) ESRS standards, but it does not meet the needs of SMEs. It is disconnected from everyday sustainability work and does not sufficiently encourage or provide practical tools for the strategic development of a company’s sustainability efforts.

One positive aspect of the standard is that it encourages companies to assess their emissions, which enables their systematic reduction. The standard can also be seen as bringing consistency and comparability to SME sustainability reporting. However, the benefit of this remains questionable if the reported information is not relevant. In its current form, the VSME risks becoming just another example of EU bureaucracy and regulation.

I recommend that SMEs pursue strategy work that is connected to and supports their core business also from a sustainability perspective. Companies should build their sustainability efforts in a business-driven and measurable way, and report on them in a manner that fits their own identity and scale. The VSME can be seen as one tool for such reporting, but it does not replace sustainability work that is linked to strategy and its appropriate reporting.

Added on 9.6.2025:Based on the VSME standard and research data the self-assessment form for sustainability work enables companies to evaluate the current state of their sustainability efforts and serves as a foundation for further development and reporting.