Corporate responsibility work is a broad and multifaceted process, especially in the early stages when a company begins building its sustainability strategy. Materiality assessment plays a crucial role in this phase, as it is neither possible nor sensible to try to address everything. Instead, sustainability efforts must focus on the most material impacts, risks, and opportunities related to the company’s operations. By concentrating on what truly matters, the company can achieve the best possible results in its sustainability work.

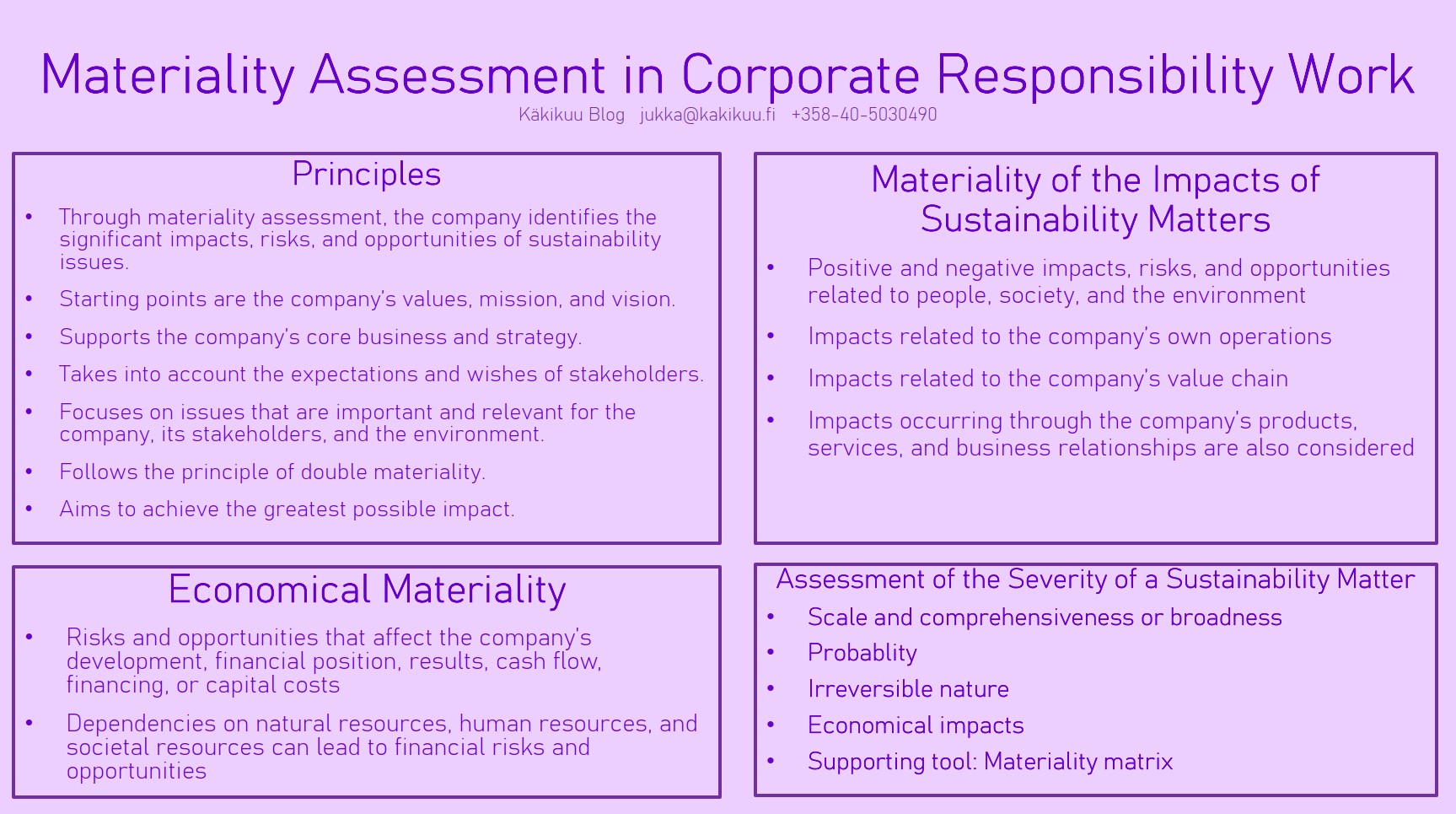

The starting points for a materiality assessment in sustainability work are the company’s values, mission, vision, and strategy. In practice, this means focusing on issues that are important to the company and support its purpose, goals, and strategic direction—i.e., matters that are truly relevant in that context. The next key step in the assessment is identifying the company’s most significant economic, social, and environmental impacts. At this stage, it is essential to consider the expectations and priorities of the company’s key stakeholders. Simultaneously, the assessment should explore the broader relevance of the identified issues—not only for the company itself, but also for its value chain, stakeholders, and society as a whole. Applicable regulatory requirements that affect the company and its operations must also be taken into account. Traditionally, materiality assessments have focused on issues the company can directly influence, but the broader impacts are increasingly seen as equally important.

The materiality assessment of a company’s sustainability work is also the starting point for sustainability reporting under the new Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS). The ESRS framework divides the materiality of a sustainability matter into two dimensions: impact materiality and financial materiality.

A matter is considered material from an impact perspective when it relates to the positive or negative effects of the company’s operations on people or the environment. In assessing impact materiality, the company must also take into account its value chain, products, services, and business relationships.

According to the ESRS standards, a sustainability matter is considered financially material if it causes or is expected to cause significant financial impacts on the company. This materiality assessment must also extend to issues over which the company has no direct control.

In itself, the definitions provided by the ESRS reporting standards do not change the traditional starting points or nature of the company’s materiality assessment for sustainability work, as described above. The main difference from previous practices is that, in the future, the assessment of the financial materiality of a sustainability matter will also need to consider issues that are outside the company’s control.

In itself, the definitions provided by the ESRS reporting standards do not change the traditional starting points or nature of the company’s materiality assessment for sustainability work.

Double materiality is a central concept in the new CSRD directive. Double materiality means that, in assessing the materiality of a sustainability matter, the evaluation considers not only the positive and negative impacts of the company’s own operations on people and the environment, but also the effects of external factors—such as stakeholder expectations or technological developments—on the company and its financial performance. In the double materiality assessment, both the impact and financial dimensions are considered, which are often interconnected. The interdependencies between these dimensions must be taken into account in the assessment.

Through the materiality assessment, a company can define the scope of its corporate responsibility work and set clear goals that are directly related to its core business. This process also allows the company to identify the impacts, risks, and opportunities associated with sustainability matters. When the scale of these factors is considered large, broad in scope, or highly likely to affect the company, they are likely to be material sustainability matters, provided they are aligned with the company’s strategy and business model. In this materiality assessment, a materiality matrix can also be used to help prioritize and determine the order of significance for these issues.

In assessing the materiality of a company’s sustainability matters, the identified and decided material sustainability issues and actions are grouped into sustainability themes, which become the focus areas of the company’s sustainability work for the strategic period. These sustainability themes should also be considered in light of the UN Sustainable Development Goals (Agenda 2030) and aligned with these objectives. This approach adds concreteness to the sustainability themes and their impact, while also integrating them into a global context of responsibility.